Fill Out a Valid IRS 2553 Form

The IRS 2553 form plays a crucial role for small business owners looking to elect S Corporation status. This election allows corporations to pass corporate income, losses, deductions, and credits directly to shareholders, thereby avoiding double taxation at the corporate level. Completing the form accurately is essential, as it requires specific information such as the corporation's name, address, and Employer Identification Number (EIN). Additionally, the form must be signed by all shareholders, ensuring their consent to the election. Timing is also critical; the form must be filed within a certain period following the corporation's formation or by the 15th day of the third month of the tax year in which the election is to take effect. Understanding the nuances of the IRS 2553 form can significantly impact a business's tax obligations and financial health, making it a vital document for those aiming for S Corporation status.

Common mistakes

-

Failing to meet the timely filing deadline. The IRS requires Form 2553 to be filed within a specific time frame to ensure S-Corporation status for the tax year.

-

Not providing accurate information. Ensure that all names, addresses, and identification numbers are correct. Mistakes can lead to delays or rejections.

-

Omitting the signature of an authorized officer. The form must be signed by someone with authority to represent the corporation.

-

Incorrectly selecting the tax year. The choice of tax year must align with the corporation's accounting period and comply with IRS rules.

-

Not indicating the number of shareholders. This information is crucial for determining eligibility for S-Corporation status.

-

Failing to include a consent statement from all shareholders. Each shareholder must agree to the S-Corporation election.

-

Not checking for additional forms or requirements. Depending on the state, there may be additional filings necessary to complete the S-Corp election.

-

Ignoring IRS instructions. Always read the instructions provided with Form 2553 carefully to avoid common pitfalls.

Preview - IRS 2553 Form

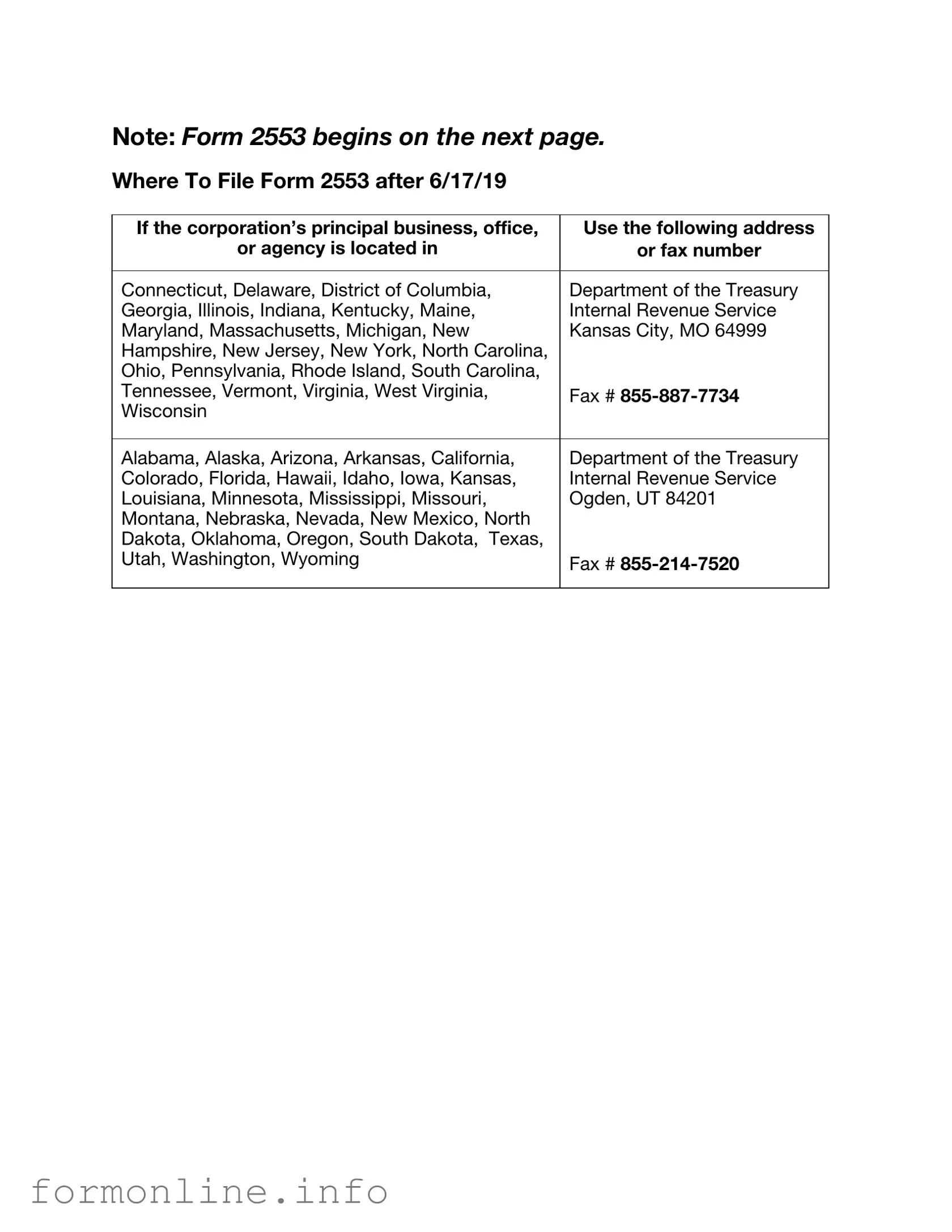

Note: Form 2553 begins on the next page.

Where To File Form 2553 after 6/17/19

If the corporation’s principal business, office, |

Use the following address |

or agency is located in |

or fax number |

|

|

Connecticut, Delaware, District of Columbia, |

Department of the Treasury |

Georgia, Illinois, Indiana, Kentucky, Maine, |

Internal Revenue Service |

Maryland, Massachusetts, Michigan, New |

Kansas City, MO 64999 |

Hampshire, New Jersey, New York, North Carolina, |

|

Ohio, Pennsylvania, Rhode Island, South Carolina, |

|

Tennessee, Vermont, Virginia, West Virginia, |

Fax # |

Wisconsin |

|

|

|

Alabama, Alaska, Arizona, Arkansas, California, |

Department of the Treasury |

Colorado, Florida, Hawaii, Idaho, Iowa, Kansas, |

Internal Revenue Service |

Louisiana, Minnesota, Mississippi, Missouri, |

Ogden, UT 84201 |

Montana, Nebraska, Nevada, New Mexico, North |

|

Dakota, Oklahoma, Oregon, South Dakota, Texas, |

|

Utah, Washington, Wyoming |

Fax # |

|

|

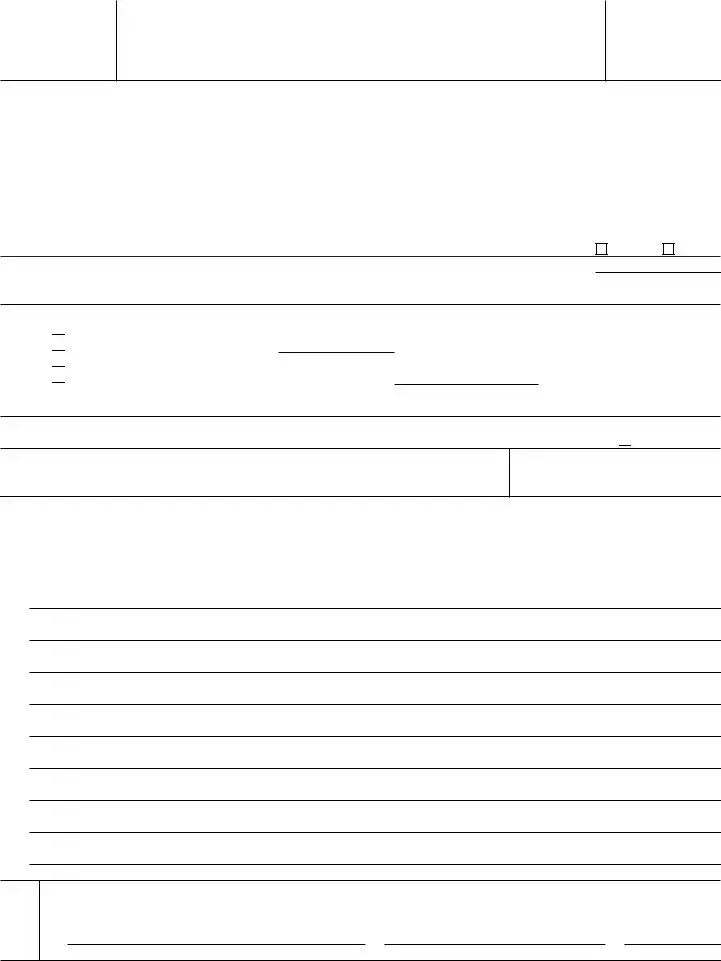

Form 2553

(Rev. December 2017)

Department of the Treasury Internal Revenue Service

Election by a Small Business Corporation

(Under section 1362 of the Internal Revenue Code)

(Including a late election filed pursuant to Rev. Proc.

▶You can fax this form to the IRS. See separate instructions.

▶Go to www.irs.gov/Form2553 for instructions and the latest information.

OMB No.

Note: This election to be an S corporation can be accepted only if all the tests are met under Who May Elect in the instructions, all shareholders have signed the consent statement, an officer has signed below, and the exact name and address of the corporation (entity) and other required form information have been provided.

Part I |

|

Election Information |

|

|

|

|

|

|

|

Name (see instructions) |

A Employer identification number |

||

Type |

|

|

|

|

|

|

|

Number, street, and room or suite no. If a P.O. box, see instructions. |

B Date incorporated |

|

|||

or |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

||

|

City or town, state or province, country, and ZIP or foreign postal code |

C State of incorporation |

|

|||

|

|

|

|

|||

|

|

|

|

|

|

|

D |

Check |

the applicable box(es) if the corporation (entity), after applying for the EIN shown in A above, changed its |

name or |

address |

||

EElection is to be effective for tax year beginning (month, day, year) (see instructions) . . . . . . ▶

Caution: A corporation (entity) making the election for its first tax year in existence will usually enter the beginning date of a short tax year that begins on a date other than January 1.

FSelected tax year:

(1) Calendar year

Calendar year

(2) Fiscal year ending (month and day) ▶

Fiscal year ending (month and day) ▶

(3)

(4)

If box (2) or (4) is checked, complete Part II.

GIf more than 100 shareholders are listed for item J (see page 2), check this box if treating members of a family as one shareholder results in no more than 100 shareholders (see test 2 under Who May Elect in the instructions) ▶

HName and title of officer or legal representative whom the IRS may call for more information

Telephone number of officer or legal representative

IIf this S corporation election is being filed late, I declare I had reasonable cause for not filing Form 2553 timely. If this late election is being made by an entity eligible to elect to be treated as a corporation, I declare I also had reasonable cause for not filing an entity classification election timely and the representations listed in Part IV are true. See below for my explanation of the reasons the election or elections were not made on time and a description of my diligent actions to correct the mistake upon its discovery. See instructions.

|

Under penalties of perjury, I declare that I have examined this election, including accompanying documents, and, to the best of my |

||

Sign knowledge and belief, the election contains all the relevant facts relating to the election, and such facts are true, correct, and complete. |

|||

Here |

▲Signature of officer |

|

|

|

Title |

Date |

|

For Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 18629R |

Form 2553 (Rev. |

|

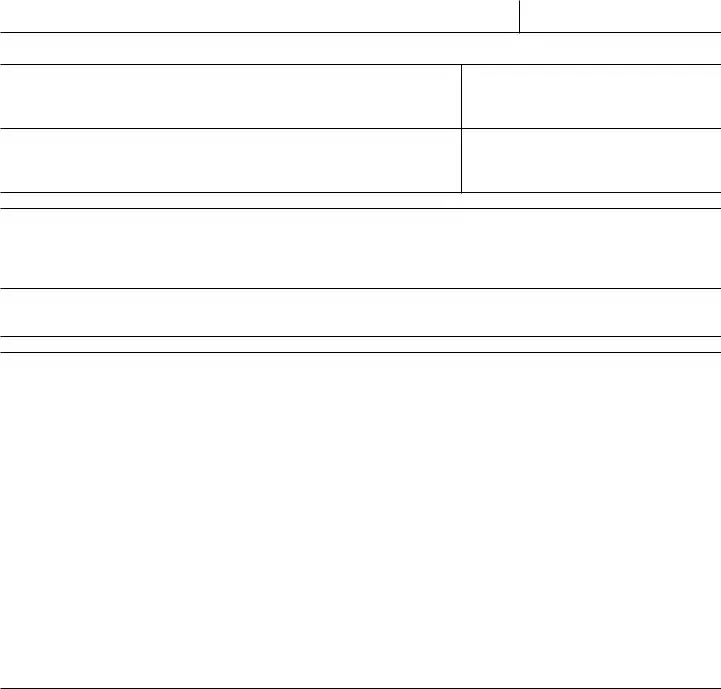

Form 2553 (Rev. |

Page 2 |

Name |

Employer identification number |

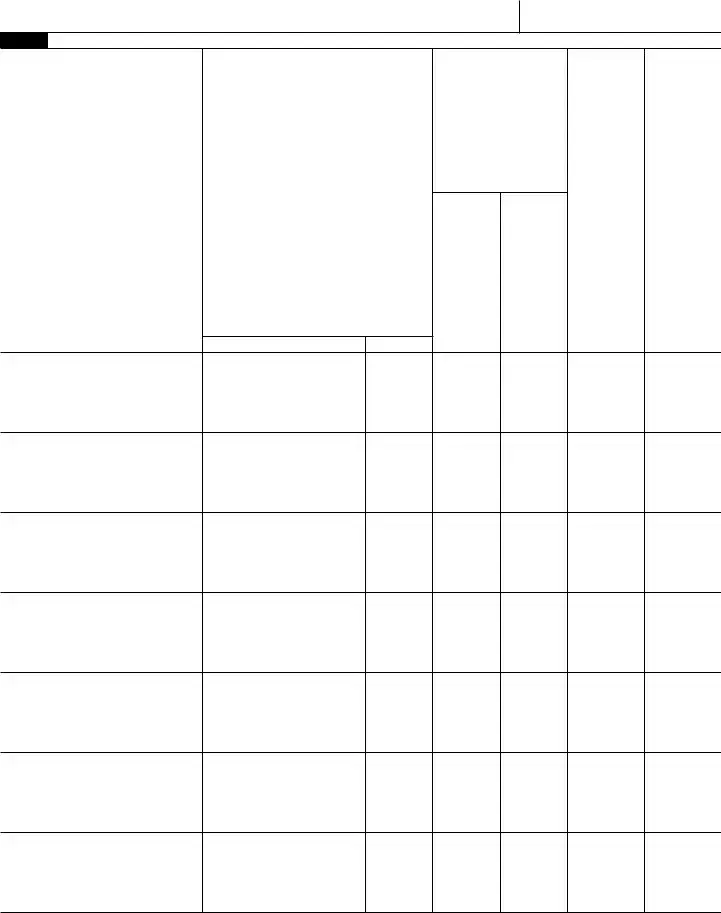

Part I Election Information (continued) Note: If you need more rows, use additional copies of page 2.

J

Name and address of each

shareholder or former shareholder required to consent to the election.

(see instructions)

K

Shareholder’s Consent Statement

Under penalties of perjury, I declare that I consent to the election of the

Signature |

Date |

L

Stock owned or

percentage of ownership

(see instructions)

Number of |

|

shares or |

|

percentage |

Date(s) |

of ownership |

acquired |

M |

|

Social security |

|

number or |

N |

employer |

Shareholder’s |

identification |

tax year ends |

number (see |

(month and |

instructions) |

day) |

Form 2553 (Rev.

Form 2553 (Rev. |

Page 3 |

|

Name |

|

Employer identification number |

|

|

|

Part II |

Selection of Fiscal Tax Year (see instructions) |

|

Note: All corporations using this part must complete item O and item P, Q, or R. |

|

|

O Check the applicable box to indicate whether the corporation is: |

|

|

1. |

A new corporation adopting the tax year entered in item F, Part I. |

|

2. |

An existing corporation retaining the tax year entered in item F, Part I. |

|

3. |

An existing corporation changing to the tax year entered in item F, Part I. |

|

PComplete item P if the corporation is using the automatic approval provisions of Rev. Proc.

1. Natural Business Year ▶ |

I represent that the corporation is adopting, retaining, or changing to a tax year that qualifies |

as its natural business year (as defined in section 5.07 of Rev. Proc.

2. Ownership Tax Year ▶ |

I represent that shareholders (as described in section 5.08 of Rev. Proc. |

than half of the shares of the stock (as of the first day of the tax year to which the request relates) of the corporation have the same tax year or are concurrently changing to the tax year that the corporation adopts, retains, or changes to per item F, Part I, and that such tax year satisfies the requirement of section 4.01(3) of Rev. Proc.

Note: If you do not use item P and the corporation wants a fiscal tax year, complete either item Q or R below. Item Q is used to request a fiscal tax year based on a business purpose and to make a

QBusiness

1. Check here ▶  if the fiscal year entered in item F, Part I, is requested under the prior approval provisions of Rev. Proc.

if the fiscal year entered in item F, Part I, is requested under the prior approval provisions of Rev. Proc.

Yes |

No |

2.Check here ▶

to show that the corporation intends to make a

to show that the corporation intends to make a

3.Check here ▶

to show that the corporation agrees to adopt or change to a tax year ending December 31 if necessary for the IRS to accept this election for S corporation status in the event (1) the corporation’s business purpose request is not approved and the corporation makes a

to show that the corporation agrees to adopt or change to a tax year ending December 31 if necessary for the IRS to accept this election for S corporation status in the event (1) the corporation’s business purpose request is not approved and the corporation makes a

RSection 444

1.Check here ▶

to show that the corporation will make, if qualified, a section 444 election to have the fiscal tax year shown in item F, Part I. To make the election, you must complete Form 8716, Election To Have a Tax Year Other Than a Required Tax Year, and either attach it to Form 2553 or file it separately.

to show that the corporation will make, if qualified, a section 444 election to have the fiscal tax year shown in item F, Part I. To make the election, you must complete Form 8716, Election To Have a Tax Year Other Than a Required Tax Year, and either attach it to Form 2553 or file it separately.

2.Check here ▶

to show that the corporation agrees to adopt or change to a tax year ending December 31 if necessary for the IRS to accept this election for S corporation status in the event the corporation is ultimately not qualified to make a section 444 election.

to show that the corporation agrees to adopt or change to a tax year ending December 31 if necessary for the IRS to accept this election for S corporation status in the event the corporation is ultimately not qualified to make a section 444 election.

Form 2553 (Rev.

Form 2553 (Rev. |

Page 4 |

Name |

Employer identification number |

Part III Qualified Subchapter S Trust (QSST) Election Under Section 1361(d)(2)* Note: If you are making more than

one QSST election, use additional copies of page 4.

Income beneficiary’s name and address

Social security number

Trust’s name and address

Employer identification number

Date on which stock of the corporation was transferred to the trust (month, day, year) . . . . . . . . ▶

In order for the trust named above to be a QSST and thus a qualifying shareholder of the S corporation for which this Form 2553 is filed, I hereby make the election under section 1361(d)(2). Under penalties of perjury, I certify that the trust meets the definitional requirements of section 1361(d)(3) and that all other information provided in Part III is true, correct, and complete.

Signature of income beneficiary or signature and title of legal representative or other qualified person making the election |

|

Date |

*Use Part III to make the QSST election only if stock of the corporation has been transferred to the trust on or before the date on which the corporation makes its election to be an S corporation. The QSST election must be made and filed separately if stock of the corporation is transferred to the trust after the date on which the corporation makes the S election.

Part IV Late Corporate Classification Election Representations (see instructions)

If a late entity classification election was intended to be effective on the same date that the S corporation election was intended to be effective, relief for a late S corporation election must also include the following representations.

1The requesting entity is an eligible entity as defined in Regulations section

2The requesting entity intended to be classified as a corporation as of the effective date of the S corporation status;

3The requesting entity fails to qualify as a corporation solely because Form 8832, Entity Classification Election, was not timely filed under Regulations section

4The requesting entity fails to qualify as an S corporation on the effective date of the S corporation status solely because the S corporation election was not timely filed pursuant to section 1362(b); and

5a The requesting entity timely filed all required federal tax returns and information returns consistent with its requested classification as an S corporation for all of the years the entity intended to be an S corporation and no inconsistent tax or information returns have been filed by or with respect to the entity during any of the tax years, or

bThe requesting entity has not filed a federal tax or information return for the first year in which the election was intended to be effective because the due date has not passed for that year’s federal tax or information return.

Form 2553 (Rev.

Other PDF Templates

Nc-4p - Individuals ceasing to be "Head of Household" do not need to file a new form until the next year.

Imm1294 Guide - Indicate the duration of your expected studies in Canada.

To simplify your delivery options, utilizing the Fedex Door Tag Authorizing Release can be particularly beneficial. This form ensures that your packages can still reach you even if you are unavailable to sign for them, as it permits the driver to leave them at a predetermined location. Make sure to fill out the form accurately and post it visibly before the designated delivery time to avoid any hiccups.

Miscellaneous Information - 1099-MISC is one of several forms in the 1099 series used by the IRS.

Documents used along the form

When forming an S Corporation, the IRS Form 2553 is essential for electing S Corporation status. However, there are several other documents and forms that are often required or beneficial to complete the process. Understanding these documents can help ensure compliance and smooth operation of your business.

- IRS Form 1120S: This is the annual tax return form specifically for S Corporations. It reports income, deductions, and credits, allowing the IRS to assess the tax obligations of the corporation.

- IRS Form 941: Employers use this form to report income taxes, Social Security tax, and Medicare tax withheld from employee wages. It is typically filed quarterly.

- IRS Form SS-4: This form is used to apply for an Employer Identification Number (EIN). An EIN is necessary for tax purposes and for opening a business bank account.

- State Corporation Registration: Each state requires businesses to register their corporation. This document ensures compliance with state laws and regulations.

- Operating Agreement: Although not always required, this internal document outlines the management structure and operating procedures of the S Corporation. It serves as a guide for decision-making.

- Shareholder Agreement: This document details the rights and responsibilities of shareholders. It can help prevent disputes and clarify the process for buying or selling shares.

- Emotional Support Animal Letter Form: To understand the significance of an essential Emotional Support Animal Letter for well-being, familiarize yourself with how this document can aid in obtaining an emotional support animal.

- Form 2553 Election Statement: In addition to the IRS Form 2553, a supporting statement may be needed if the corporation is filing late. This statement explains the reason for the late election.

- State Tax Forms: Depending on the state, additional tax forms may be required for compliance with state tax laws. These forms vary widely and should be researched based on the corporation's location.

Filing the IRS Form 2553 is just one step in establishing an S Corporation. By understanding and preparing the associated documents, business owners can help ensure that their company operates smoothly and remains compliant with both federal and state regulations.

Similar forms

The IRS Form 1065 is used by partnerships to report income, deductions, gains, and losses from the operation of a partnership. Like Form 2553, which is used to elect S Corporation status, Form 1065 allows entities to pass through income to their partners. Both forms require detailed information about the entity and its financial activities, ensuring that the IRS has a clear understanding of the business structure and its tax implications.

Form 1120 is the U.S. Corporation Income Tax Return. Corporations use this form to report their income, gains, losses, deductions, and credits. Similar to Form 2553, which allows corporations to elect S Corporation status, Form 1120 is essential for C Corporations to fulfill their tax obligations. Both forms require accurate reporting of financial data, but they cater to different types of corporate structures and tax treatments.

The IRS Form 8832, Entity Classification Election, allows businesses to choose how they want to be classified for federal tax purposes. This form is similar to Form 2553 in that both allow entities to elect their tax status. While Form 2553 is specifically for S Corporations, Form 8832 provides a broader choice, enabling businesses to select between being classified as a corporation, partnership, or disregarded entity.

In the context of hiring and partnerships, the Employment Verification form plays a vital role in corroborating a potential employee's professional background, much like the significance of tax classification forms such as Form 1065. Employers must ensure they gather all necessary documentation to avoid misunderstandings and streamline their recruitment processes; for further assistance, refer to Top Forms Online, which offers resources on employment verification.

Form 941 is the Employer's Quarterly Federal Tax Return. Employers use this form to report income taxes, Social Security tax, and Medicare tax withheld from employee wages. While it serves a different purpose than Form 2553, both forms are crucial for compliance with IRS regulations. They require accurate reporting of financial information and have specific deadlines that businesses must meet to avoid penalties.

Form 1065-B is the U.S. Return of Income for Electing Large Partnerships. This form is similar to Form 2553 in that it caters to specific types of partnerships that elect to be treated differently for tax purposes. Both forms facilitate the pass-through taxation model, allowing income and losses to be reported directly on partners' tax returns, rather than being taxed at the entity level.

Form 1120-S is the U.S. Income Tax Return for an S Corporation. This form is directly related to Form 2553, as it is used by entities that have elected S Corporation status. Both forms are interconnected; Form 2553 is the election, while Form 1120-S is the return that must be filed annually. This ensures that S Corporations report their income and deductions accurately, reflecting their unique tax treatment.

Form 8862 is the Information to Claim Certain Refundable Credits After Disallowance. While this form deals with claiming specific tax credits, it shares similarities with Form 2553 in that both require detailed information and documentation to support claims made to the IRS. Each form plays a role in ensuring compliance and proper reporting, although they serve different purposes within the tax system.

Dos and Don'ts

When filling out the IRS Form 2553, it's crucial to follow specific guidelines to ensure your application is processed smoothly. Here are some important dos and don'ts to consider:

- Do provide accurate information. Double-check names, addresses, and other details.

- Do file the form on time. Submit it within 75 days of your corporation's formation or by the tax year deadline.

- Do ensure that all shareholders consent to the S Corporation election. Their signatures may be required.

- Do keep a copy of the completed form for your records. This can be helpful for future reference.

- Don't forget to include the correct tax year. Specify the year for which the election is intended.

- Don't submit the form without reviewing it thoroughly. Errors can lead to delays or rejection.

Key takeaways

Filling out and using the IRS 2553 form is a critical step for small businesses wishing to elect S Corporation status. Here are five key takeaways to consider:

- Eligibility Requirements: Ensure your business meets the eligibility criteria for S Corporation status. This includes having no more than 100 shareholders and only one class of stock.

- Filing Deadline: Submit the IRS 2553 form within 75 days of the beginning of the tax year in which you want the S Corporation status to take effect. Missing this deadline can result in a delay or denial of your election.

- Shareholder Consent: All shareholders must sign the form to indicate their consent to the S Corporation election. This requirement underscores the importance of clear communication with all stakeholders.

- Tax Implications: Understand the tax implications of electing S Corporation status. This election allows income to pass through to shareholders, potentially reducing the overall tax burden for the business.

- Amendments and Revocations: Be aware that once the election is made, it can be revoked or amended under certain conditions. Familiarize yourself with the process to ensure compliance and maintain your desired tax status.

Taking these factors into account can help ensure a smooth and compliant election process for your business.

How to Use IRS 2553

Filling out the IRS Form 2553 is an important step for businesses looking to elect S Corporation status. This process requires attention to detail and accuracy to ensure that the form is submitted correctly. Follow the steps below to complete the form efficiently.

- Download the IRS Form 2553 from the official IRS website.

- Begin by entering the name of your corporation at the top of the form.

- Provide the corporation's address, including city, state, and ZIP code.

- Enter the date of incorporation in the designated field.

- Indicate the tax year the corporation will use, typically a calendar year.

- List the names, addresses, and Social Security numbers of all shareholders.

- Specify the number of shares owned by each shareholder.

- Complete the section that asks about the corporation’s eligibility for S Corporation status.

- Sign and date the form. Ensure that an authorized officer of the corporation signs it.

- Submit the completed form to the appropriate IRS address based on your location.

After submission, the IRS will review your form and notify you of the acceptance or any issues. It's advisable to keep a copy for your records and follow up if you do not receive confirmation within a reasonable timeframe.